The third phase of 5G main equipment promotion "volume increase and price reduction", China's 5G construction presents three major changes

The biggest popularization of the third phase of 5G main

equipment is "volume increase and price reduction". China's 5G

construction performance characteristics: network coverage demands higher than

high-speed access, lower operation and maintenance costs demand far-reaching

access capabilities, and 5G investment is shifting from wireless main equipment

to other directions.

China Unicom’s 5G wireless master equipment (2.1G) four times

China promotion results were released, so far the operator’s 5G third phase

wireless master equipment popularization has been completed. The characteristic

is "volume increase and price reduction". China's 5G construction is

showing major changes: network coverage demands greater high-speed access,

operation and maintenance costs demand other access reductions, and 5G is

shifting from wireless main equipment.

The IDC report pointed out that in 2021, operators snapped

up 722 thousand main wireless equipment stations (including China Mobile and

China Radio and Television's 48,700 million 5G base stations completed in two

years), and the investment amount exceeded 580 yuan. Compared with the second

phase of 5G last year (the three companies have increased by 480,000 stations,

and the investment amount is 700 yuan), the obvious change is "volume

increase and price decrease."

In addition, the entry and exit of equipment vendors and

market changes in this popularization are the focus of market attention, but

IDC believes that the future impact of technology and product prompts on

China's 5G construction is more important. On the whole, I believe that IDC has

the following three major changes:

Network coverage demands greater high-speed access. Network

coverage demands greater high-speed access. The effective equipment popularized

this time is driven by the 5G base station 700M from China Mobile, while the

telecommunications 5G base station uses 2.1G bandwidth. The use of lower pixels

can increase the network coverage and depth. This is also the inevitability of

improving 5G network services, thereby increasing An important way of existing

5G user experience. In addition, 2.6G and 3.5G continue to be used to cover the

areas of interest in the city (not overlapped with coverage).

Judging from the unit price of the latest equipment promoted

this time, combined with the equipment capacity of this promotion, it can be

fully converted from 32T32R/64T64R last year to 4T4R, which will fatally reduce

baseband consumption and reduce operation and maintenance costs.

5G investment is shifting from wireless main equipment to

other directions. Due to the model and parameters of the wireless main

equipment purchased in the third phase of the 5G and the trend of change, the

unit price of the equipment is not much contrasted, but overall, under the

premise of a small increase in the overall investment scale of 5G, the 5G

investment in the G wireless main equipment is decreasing. More 5G capital

expenditures are used in other areas, such as online networks, core networks

and 5G private network solutions.

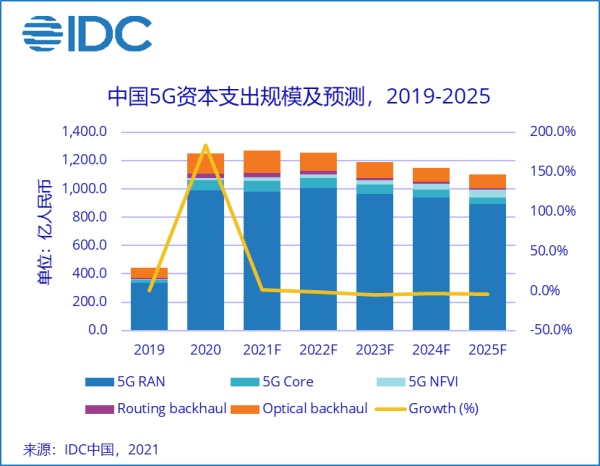

Market changes and adjustments, IDC according to the

"China 5G Capital Forecast, 2021-2025" report, and from 5G wireless

access network, 5G core network, 5G function virtualized network

infrastructure, 5G data communication and 5G optical backhaul Refinement and

prospects for 5G in 5 dimensions.

IDC believes that China's 5G CAPEX market will have firm

beliefs. Looking at the status quo of 5G in China, despite the rapid growth of

5G construction in 2020, combined with a number of comprehensive considerations

such as technology, policy, commercialization, and industry standards, IDC

believes that China's 5G will not happen overnight. 5G development will play a

role in the application of 5G industry. With continuous deepening and

fermentation, the 5G construction speed investment plan of Chinese operators is

freely advanced, and the investment direction is adjusted annually to the needs

of the urban development market. It is believed that through the continuous

exploration and innovation of Chinese enterprises, operators and equipment

vendors, China will continue to lead the development of the global market in

terms of 5G construction and applications.

IDC China Telecom and Internet of Things Research Assistant

Researcher Lei Kai said: "Looking forward, China's four major operators

will maintain the continuity of 5G network investment, continue to promote the

reduction of 5G network equipment unit prices, explore 5G application business

models, and improve 5G networks 5G. High-speed network investment and return on

investment. The high-speed investment of 5G network and the speed of 5G

application development. New industry markets, the development of digital

economy, especially the rise of business models after the new crown epidemic,

5G will become an important market killer in the digital transformation of the

industry The first phase of technology. The transformation of commercial

services to help operators overcome the operating pressure of being'pipelined'

is also the core driving force for 5G construction."