The SD-WAN market is booming with strong entry

The development of cloud computing, big data, AI and other technologies has promoted the digital transformation of enterprises, as well as online applications, big data analysis and concurrent processing, AR/VR and other scenarios, the traditional enterprise network solutions are facing the network infrastructure complexity, network architecture closure, end-side application experience poor series of challenges. In order to reduce the cost of network construction, ensure business experience and improve operational efficiency, a new network technology scheme SD-WAN has emerged. With the maturity of SD-WAN technology, with its strong advantages and market prospects, attracted a lot of manufacturers to enter, fierce competition.

First, SD-WAN definition, product form and customer scene

1.1 SD-WAN definition

SD-WAN is an important branch technology of software-defined network, which generally refers to the sophisticated software technology (intelligent dynamic routing control, data optimization, TCP optimization, QoS) and traditional network resources (such as public Internet) to maximize the performance of traditional network resources, so that users can intelligently manage WAN bandwidth on their own. Through the use of software-defined network technology, users can independently control the flow of WAN traffic according to the predetermined routing strategy, integrate MPLS line, fiber optic, Internet, LTE and other network line resources for WAN traffic scheduling, to achieve the network quality of ordinary interconnected links to reach the special line, reduce traffic costs, improve bandwidth utilization; At the same time, for multiple sites, according to the current network situation and configuration strategy, automatically choose the best path, to achieve load balancing, to ensure the network-wide network quality.

1.2 SD-WAN product form.

SD-WAN comes in a variety of product forms, from physical or virtual devices to remote branch offices, or to service-based products on a cloud platform. SD-WAN's product patterns at this stage can be broadly divided into three types:

Software products: SD-WAN abstracts the underlying physical transport layer in a software-defined manner, integrates and harmonizes a wide variety of physical links, and provides applications with highly available and high-performance virtual WAN services. Service providers can implement the various functions of SD-WAN services on the user side through the way of the subordinate software. The advantages of software products are cost-saving, no need to customize the terminal, flexible deployment, according to the requirements of enterprises to do customized development.

Hardware products: SD-WAN software curing into custom hardware terminals, to hardware terminal product form to provide customers. Terminals according to the customer's region, by the service provider in advance to do a good job of the relevant parameters configuration, Internet network to achieve plug and play, zero configuration. The advantage of hardware products is that they are quick to deploy and easy to deliver. In addition, hardware products have a certain failure rate, maintenance services will add additional costs.

Service products: SD-WAN is finally reflected in the user side of the complete set of services, to help customers in the control of costs under the premise of meeting its diverse, high-quality service requirements. As a result, SD-WAN complete solutions can be packaged into service products for customers based on specific needs. Such service offerings can include basic bandwidth resources, customized resource allocation for customer-specific business needs, or the provision of all-in-one managed services.

1.3 Target audience and scene

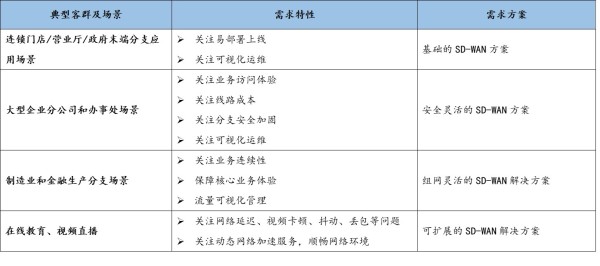

SD-WAN includes several typical scenarios such as chain store branch applications, large enterprise branches/offices, manufacturing/finance branches, and live video. In different scenarios, the customer's requirements characteristics and demand scenarios are different. This is shown in the table below.

Second, SD-WAN market space

2.1 SD-WAN market size

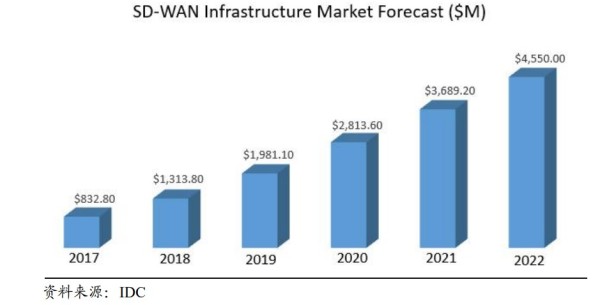

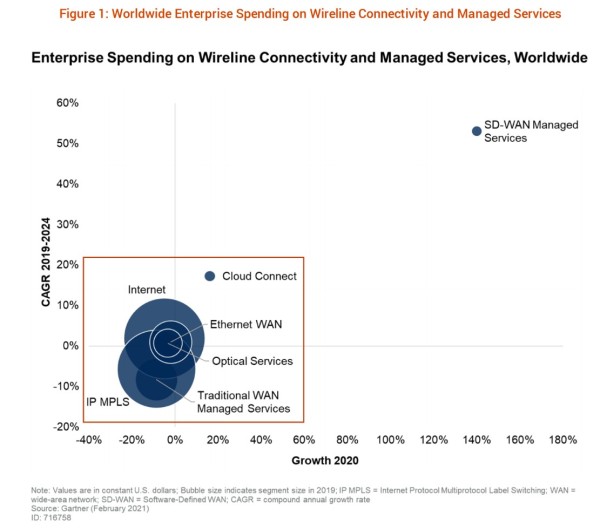

SD-WAN market scale growth, the future prospects for development. According to IDC, the size of the SD-WAN infrastructure market grew from $832 million in 2017 to $4.5 billion in 2022, with a five-year compound growth rate of 40%. In terms of managed services, Gartner predicts that SD-WAN managed services will grow at a CAGR of 53% over five years and 140% annually in 2020.

2.2 SD-WAN Advantage Analysis

SD-WAN's broad market prospects depend on its strong strengths. SD-WAN simplifies wan management and operation by separating network hardware from its control mechanisms, allowing companies to use low-cost Internet access to build higher-performance WANs and replace some or all of the expensive WAN private links, such as MPLS. Compared to traditional special lines, SD-WAN products have several outstanding advantages.

1, unified management platform. Controllers in SDNs allow all SD-WAN devices to be managed and configured without the need to manage each device individually in the traditional way.

2, user experience improvement. If the line fails, the controller can switch lines based on the state perceived by the application layer, which the user does not feel throughout the process.

3, cost-effective. It can not only get the stability of the private network, but also enjoy the cheap bandwidth of ordinary Internet lines. Cisco predicts that SD-WAN will save at least 30% per year compared to the private network at the same scale of bandwidth.

4, save a lot of operational costs.

5, connect virtualization applications unified deployment.

6, can achieve visual management.

Third, SD-WAN industrial ecology

3.1 SD-WAN market player

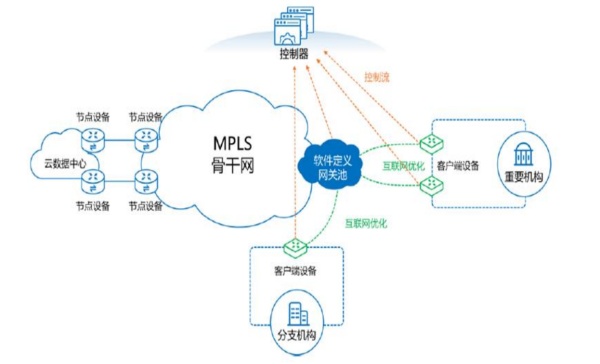

Globally, SD-WAN is regarded by many companies as a "rookie" in the industry because of its agility, security, reliability, flexibility, diversity and many other characteristics. Thus in the SD-WAN industry ecology, many enterprises have emerged, including operators, network equipment manufacturers, service providers, etc. , as shown in the figure below.

(1) Telecommunications operators

Telecom operators based on their own rich, high-quality trunk network IP technology, fusion network for enterprises to provide branch site interconnection and dedicated line services, the main enterprises are China Mobile, China Telecom, China Unicom, AT-T, Orange and so on.

(2) Service provider Service providers provide SD-WAN access services, information services, cloud services, etc. to enterprise users based on typical customer needs and business scenarios, including Tencent Cloud, AWS, Google Cloud, Aryaka, and more.

(3) Scheme provider

Solution providers are committed to providing SD-WAN applications and overall solutions for business informatization in key industries such as government, finance, and education.

(4) Equipment provider

Equipment providers mainly provide enterprise users with SD-WAN required software and hardware equipment, its SD-WAN products are based on the original enterprise CPE equipment NFV, or the original WAN network equipment SDN, on behalf of enterprises such as Huawei, Versa, ZTE, Convinced Service, Dell and so on.

(5) Chip provider

Chip providers mainly provide enterprise users with hardware chip accessories, the main enterprises are Intel, Shengke and so on.

(6) Third-party organizations

Based on the SDN needs of operators/enterprises/data centers, third-party organizations set standards, technology development, industrial development and ecological construction for SDN architecture, south-facing interface, north-facing interface, SDN security, etc., mainly CCSA, ONUG, etc.

(7) Open source community

Open source communities, with the principle of open innovation, have significantly lowered the threshold for technology suppliers, made technology transparent, and accelerated the evolution of SD-WAN technology, with GitHub and others in key communities.

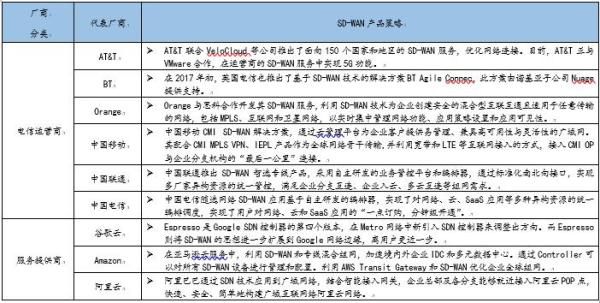

3.2 Typical vendor SD-WAN development strategy

Many manufacturers enter the SD-WAN market, to provide SD-WAN products and services, its development focus is different, more manufacturers from their own business to provide SD-WAN services. For example, telecom operators combine SD-WAN services with backbone management, and cloud service providers provide SD-WAN services from cloud service scenarios. A comb of the specific vendor SD-WAN product strategy, as shown in the table below.