The days of exponential 5G capex growth are over but the outlook is not bleak

2022.09.03

The days of exponential 5G capex growth are over but the outlook is not bleak

The 5G FWA business case is expected to be gradually challenged as the ratio between mobile network and dedicated FWA capex evolves to address the inherent capacity constraints of mobile networks, but there is still plenty of room to grow.

Stefan Pongratz, vice president and analyst at market research firm Dell'Oro Group, recently published a commentary on the progress of the 5G cycle. He noted that with the RAN market seeing its first quarterly year-over-year decline in more than two years and 5G RAN growth slowing in Q2 2022, understanding where we are in the 5G cycle will allow us to better assess Future growth prospects, this is very important.

Here's the full content of Stefan Pongratz's review article:

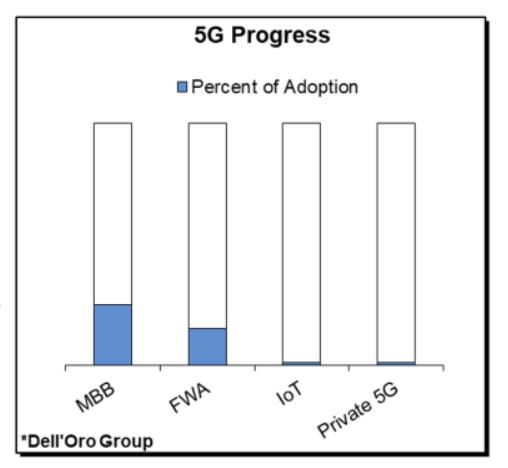

The growth of 5G enhanced mobile broadband (eMBB) is surprising from a coverage and consumer adoption perspective, as 5G NR is two to three years ahead of LTE.

However, although 5G currently accounts for the largest share of RAN capex, from a global coverage perspective, the development of 5G technology covering about 25% of the world's population (Ericsson data) is still in its early stages. The cumulative 5G NR shipments in 2019-2021 are also around 25% relative to the expected 5G NR macro site installation base in 2026.

Additionally, beyond initial coverage, more investment is required to support all frequency bands, including sub-1GHz, 2GHz, 2.5-6GHz, 6-7GHz, and mmWave. So far, operators have mostly focused on the upper part of the mid-band. The advantages of the other four bands remain significant, extending the life of the 5G investment cycle.

In addition to MBB, Fixed Wireless Access (FWA) use cases are also growing at a healthy pace, contributing to the evolution of 5G. 5G FWA is currently in the early stages of adoption, with about a third of the more than 200 commercial 5G networks offering 5G FWA services (GSA data).

The 5G FWA business case is expected to be gradually challenged as the ratio between mobile network and dedicated FWA capex evolves to address the inherent capacity constraints of mobile networks, but there is still plenty of room to grow. 5G FWA subscribers are expected to account for nearly 6% of global broadband connections by 2026, up from less than 1% in 2021 (Ericsson, Dell'Oro data). The FWA RAN market will roughly double in the next five years.

Not surprisingly, at this node, 5G private networks and NR IoT don't contribute much to broader 5G RAN revenue.

While there are significant 5G RAN opportunities in both public and private NR IoT, the market is still in its early stages. It will take some time for them to come out of the hype and capture a larger share of the RAN market (LTE+5G private network small cell market revenue is expected to reach $800 million to $1 billion by 2026).

In conclusion, we are not overly concerned about the recent slowdown in growth. 5G is still in its second phase, and we have repeatedly emphasized that the 5G cycle will be longer than the previous technology cycle. On this point, our opinion has not changed.

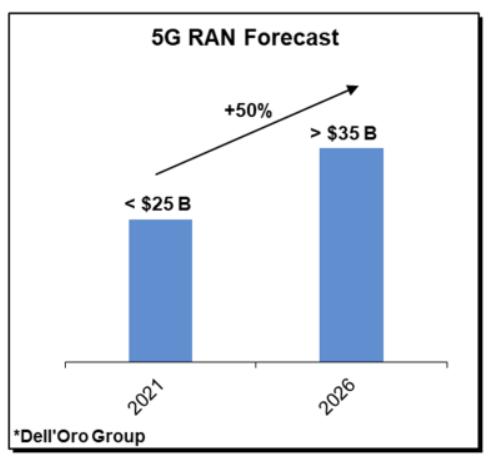

In other words, the days of exponential 5G capex growth are over, however, the 50% potential growth rate of the 5G RAN MBB, FWA and IoT markets over the next five years should be something to celebrate.